After the bursting of the pandemic biotech bubble, talk of industry consolidation was ubiquitous. The sector had pushed out too many IPOs during the go-go years, leading to too many public biotech companies, with sub-scale enterprises, and wasteful crowding in lots of therapeutic categories. And too many inexperienced management teams leading those newly-minted public companies. There’s certainly some truth in those claims.

Many industry insiders tried to push for consolidation, including encouraging both outright acquisitions and mergers of equals, to try to streamline and “right-size” the sector. And if consolidation didn’t work, struggling companies were encouraged to consider just throwing in the towel and move to shutdown, returning the remaining cash to shareholders via liquidation. White papers were written and shared widely about these points. Some investors even hosted “brainstorming” events with groups of CEOs to try to facilitate dialogues about meaningful and productive combinations. Such was the prevailing sentiment in early 2022.

So what happened in the nearly two years since then?

Well, very little consolidation, if any.

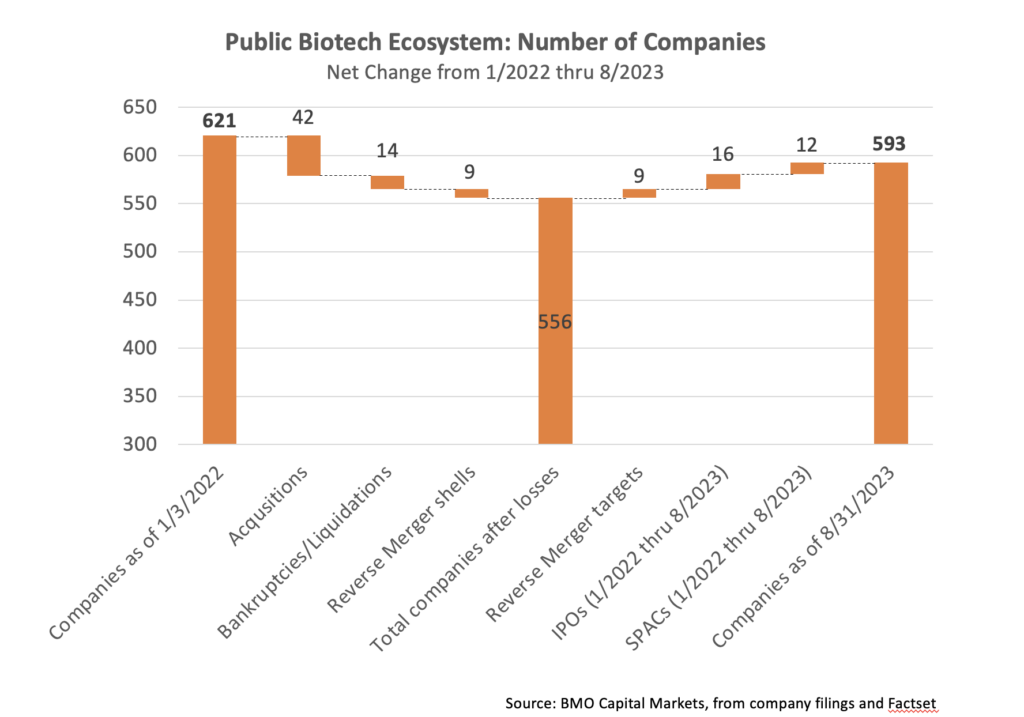

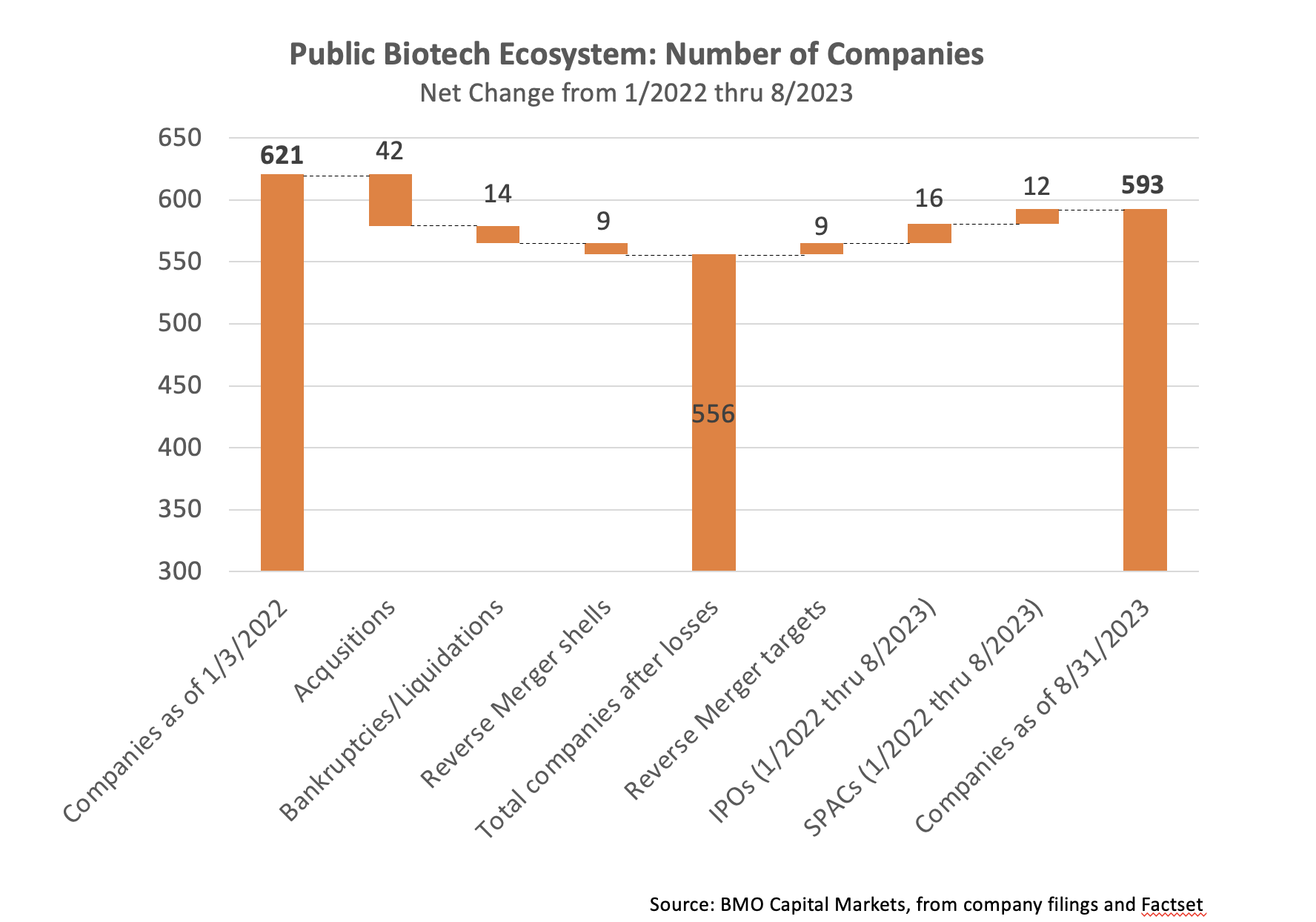

Several years into the post-bubble bear market, the public biotech sector has only contracted by 4.5% since early 2022. Here are the data from BMO Capital Markets, looking at the changes to the overall public market company counts:

Shutdowns were only 2% of the sector: declaring failure and closing up shop just hasn’t happened often. M&A, including by Pharma or via mergers of equals, only happened for 7% of the companies in the sector. “Bigger players eating smaller players” in the public markets just doesn’t happen with enough frequency to dent the broader number of publicly traded companies. The net change in past two years, in light of about thirty new public biotechs (IPOs and SPACs), was a slim 28 companies out of ~600.

It’s worth noting that reverse mergers don’t shrink the sector – they just put a private surviving story into the public shell of a dying one. Furthermore, reverse mergers are often seen as an attractive alternative to shutting down as it keeps hope alive – and pays bankers some fees during this IPO famine (that typically aren’t paid in liquidations or wind-downs).

As a historical comparison, in the post-Genomics-Bubble aftermath from 2001-2003, the public biotech sector only shrank 7% despite similarly loud calls for consolidation, according to data in E&Y Reports from that time. A much bigger drop happened in the Great Financial Crisis, where we saw a net reduction of nearly 20% of the public biotech arena between 2007-2009. A hangover from an overly euphoric technology bubble is very different, perhaps, than the contagion of a financial system meltdown, at least in terms of driving biotechs to disappear.

So why has it been so hard to drive consolidating deals or liquidations, either now or in the post-2001 aftermath?

Perhaps the sector just isn’t well-suited to broad restructuring and consolidation. Hype, hope, and finding a way just keep companies going (even if it’s not great for existing shareholders). The only time a big shift in the number of biotechs happened was when the financial markets ground to a halt, with banks going under, in the GFC – and that was only 20%, as noted above. My guess is most industry insiders would like to see 30-40% fewer public biotechs. I’m fairly confident that’s not going to happen anytime soon.

A few thoughts as to why there are so few consolidating combinations and shutdowns:

- It’s always about the people. Mergers of Equals require both management teams, in particular CEOs, and their Boards to come to agreement around who will survive to lead the merged enterprise. For CEOs and other executives who’ve invested tirelessly in these companies for years, sometimes as founders, the idea of handing the reigns to others is often emotionally charged and challenging. And Boards often back up their own management teams in these discussions. So it’s a tricky dance, and these softer issues can greatly distort the objectivity of the analysis around the combination. One of the few times this does work is when the biggest shareholders in both parties are the same firms, and thus are able to push and pull from both sides of a deal.

- Making the math work can be hard. There’s always a debate about what the relative value should be in a corporate combination, but it’s especially relevant when the market cap is way below the cash on the balanced sheet (negative EV), or where there’s some large dislocation with regard to residual asset value. While there are reasonable guardrails on the premium paid due to market expectations and disclosure requirements, these can still create an impasse for getting deals done – even when there are few alternatives.

- Public boards don’t often have significant owners (or activists) in the room, especially with more “seasoning” as public companies. Sadly, Owner-Directors with significant stakes in companies generally transition off of public Boards (e.g., VCs are paid to make new deals, not sit forever on public Boards). That’s an important and much broader topic for a future blogpost, but the immediate consequence in this setting is that “existing shareholders” who might benefit from a wind-down more so than a reverse merger (or continuing to burn money chasing futile programs), are sometimes less well represented. Activists like Kevin Tang at Concentra have been very engaged in a number of situations recently, which can change the discussion (like it did for Jounce Therapeutics).

- Zombies often find ways to continue to stay “alive”. The reality is biotech is full of “zombies” – microcap public companies that never seem to die, as the New York Times described way back in 2007, and simply survive by continually washing out prior shareholders with the optimism of new investors. Never quite raising enough to deliver, but also never dying. Once you’re trading on the public markets, there’s frequently another bottom-feeding investor willing to recap the company and keep it going – getting in at a great price but of questionable quality. Sometimes it works, though, and that’s what keeps the hope alive.

While there’s little to show for two years of the “we need fewer public biotech” sentiment, there’s obviously going to be some temporal dynamic in these data. Companies that raised follow-on financings in the better days of 2021 are likely running on fumes now; they will either raise capital or fall into one of these other categories: Acquisition, Reverse Mergers, MOEs, shutdowns, or bankruptcies – or they will have to partner their prize assets and start over. And many have been “kicking the can down the road” through RIFs and portfolio prioritizations, which may or may not “work” at creating a path to successful survival during this challenging period. So there’s still some time left for the public biotech world to meaningfully shrink. That said, there’s also a huge backlog of later stage privates that have tapped out venture and want to access the public markets – which is likely to offset some of the contraction from existing public companies.

The bottom line is that big changes in industry numbers via consolidation/shutdowns are rather unlikely to happen. Convincing a management team and/or their Board to just shut down or hand the keys to someone else is superbly hard. It happens sometimes, but nowhere near as much as it probably should. Which is why we’re likely stuck with a big universe of small cap public biotech companies for the foreseeable future.

{kind=link}